Why Credit Card Utilization Matters More Than You Think

The credit scores are a mystery, however, there is one that somewhat is orchestrating it more than most individuals are aware of. The importance of credit card usage is even greater than you might have guessed is based on the judgment of lenders. Although you can pay on time every time, it is also possible to hurt your score by utilizing excessive amounts of your available credit. The use of credit is in reality the second credit-scoring element after payment history.

Learning about Credit Card Usage.

What Does credit card utilization mean?

The use of your available revolving credit is known as the credit card utilization. It is determined by the amount of your credit card divided by the sum of your credit limit.

Example:

- Credit limit: $5,000

- Balance: $1,500

- Utilization: 30%

This is a straightforward ratio with strong messages to the lenders in regards to your debt management.

Over latest post:Best Credit Score Range for Personal Loans and Credit Cards Proven Guide (2025)

Computation of Utilization.

- Credit scoring models consider:

- Use of cards individual (one card at a time).

- Utilization (total aggregate of all cards)

Both matter. It is possible to score badly even when you maximize the use of a single card to look reasonable.

The reason why the use of credit cards is more important than you suppose.

Most individuals tend to believe that it is sufficient to pay the bills on time. Although that is necessary, utilization constitutes approximately 30 percent of the majority credit scores. A high utilization implies a financial burden whereas a low utilization implies control and stability.

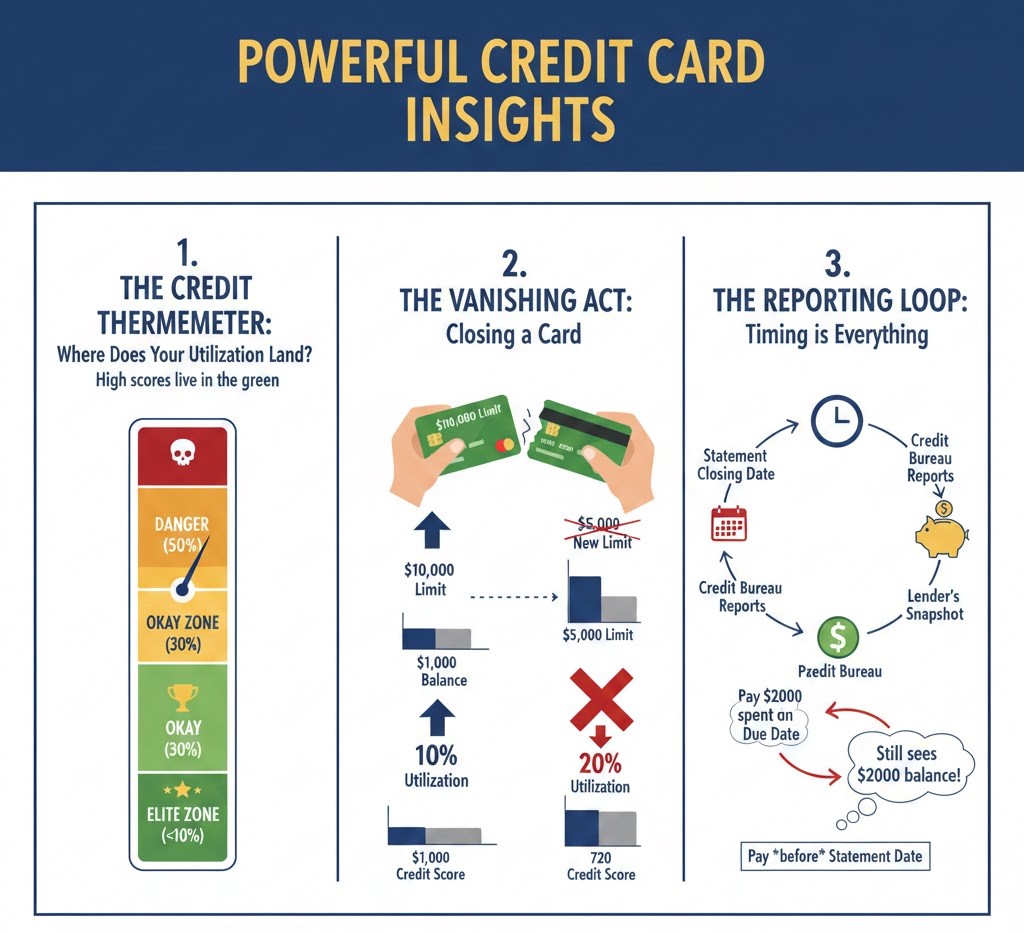

The 30% Rule Explained

The most frequently used rule is to maintain utilization at less than 30% although less is preferable:

- Under 10%: Excellent

- 10–30%: Good

- Over 30%: Risky

Violating this line even in the short term may lead to observable decreases in the score.

Individual vs General Utilization

When a single card is close to its limit, the lenders could take it as a red flag. That is why the use of credit card is an issue that is worth considering than you expect even when you have small balances that might appear manageable.

Over latest post:How a Bad Credit Score Affects Loan Approval – 17 Powerful Facts Lenders Don’t Tell You

Credit Utilization and Credit Scores

Impact on FICO Scores

Utilization is given a great weight by FICO scores. Having high balances can indicate that you can be overdepending on credit and perceived risk is higher- even with perfect pay-out history.

Impact on VantageScore

VantageScore has also given more emphasis on utilization and it can update more frequently and so your score can increase or decrease rapidly depending on the new balances.

Real-World Examples

Consider two borrowers:

- Borrower A: Utilization of 15 per cent, credit score of 725.

- Borrower B: 50% utilization, 680 credit rating.

Both make payments on time but Borrower A is eligible to better rates and quick approvals. This life experience demonstrates well why the use of credit cards is important to you than you imagined.

Loan Approvals and Utilization of Credit.

Mortgages

The utilization is scrutinized closely by the mortgage lenders. Increased ratio may decrease the chances of approval or raise interest rates and cost thousands in the long-run.

Auto Loans

The frequent outcomes of high utilization include:

- Higher APRs

- Stricter loan terms

- Personal Loans

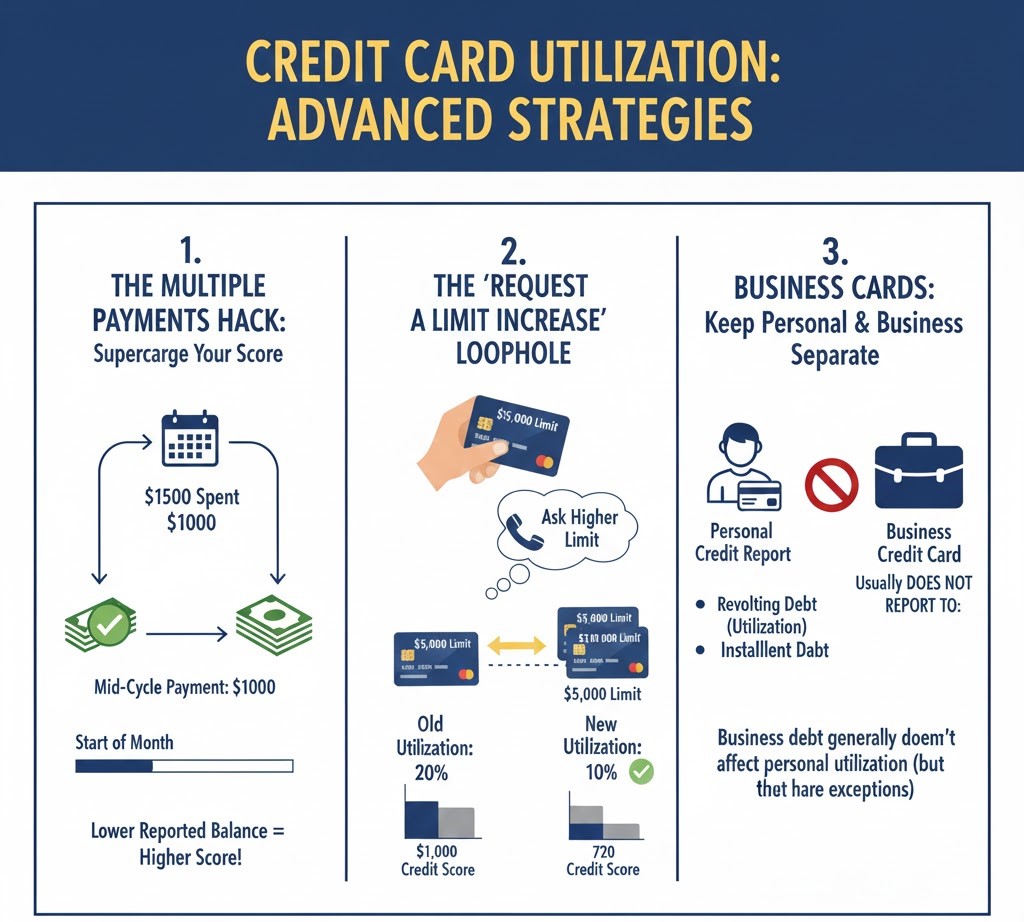

These loans are often unsecured hence lenders depend on utilization much to determine risk.

Over latest post:How Health Insurance Really Works in the USA 2026

Behavioural Indications Behind Utilization.

High utilization can signal:

- Overdependence on credit

- Lack of emergency savings

- Inconsistent budgeting

These trends are cautious to lenders even when the income is steady.

Behavioural Indications Behind Utilization

High utilization can signal:

- Overdependence on credit

- Lack of emergency savings

- Inconsistent budgeting

These trends are cautious to lenders even when the income is steady.

Popular Myths of Usage of the credit

- Myth: Avoiding utilization problems by paying in full.

- Fact: What you have on your statement date counts.

- Myth: Utilization damage is eternal.

- Fact: Usage is re-combinable every month.

These myths can be used to understand why the use of credit card is so significant than you believe.

Recommendations on how to reduce utilization provided by experts.

Pay Balances Prior to Closing of Statement.

- Early payments are a guarantee of reduced reported balances.

- Demand Credit Limit Increases.

- The increased limits may lower the utilization, as long as expenditure does not rise.

- Dispersing the expenditure on cards.

- Even distribution of cards can be used to ensure low individual utilization.

Over latest post:How Personal Loan Interest Rates Are Calculated in the USA 2026

Timing is Everything as more people think

Credit bureaus normally set balances on your account closing date and not your due date. The payment before such date can make your utilization and score fast.

Utilization of credit in the case of emergency.

Underutilization can be overcome by short-term emergencies. If this happens:

- Settle balances within the shortest time possible.

- It is better not to apply to new credit immediately.

Any future gains in the short term can be recouped through a clever planning.

Measuring and controlling Usage Tools.

Helpful tools include:

- Credit bureau apps

- Bank mobile apps

- Budgeting software

These tools assist you in remaining below important thresholds and not being in a surprise.

Frequently asked questions (FAQs).

Why is the use of credit cards as important as you think?

It has a serious effect on credit ratings and interest rates as well as loan access.

What is the best utilization ratio?

Ideally, it should be below 10 per cent whereas acceptable is below 30 per cent.

Is there an effect on utilization with paying in full?

No. It is statement balances that get reported.

What is the rate at which utilization can increase my score?

Typically in a single billing cycle.

Will high utilization be detrimental even in case of perfect payments?

Yes. The history of utilization and payment are different.

Does more emphasis lie on utilization than on payment history?

No it usually is the second most important factor.

Conclusion

The awareness that the use of credit cards is more than just a big deal helps you to score big. Most people do not anticipate the impact that it has on your credit score, loan approvals, and borrowing. With balances and timing and strategic use of credit, you will be able to secure your score and open up more promising financial prospects.