Whole vs Life Insurance Term- Which is financially viable?

One of the most significant financial decisions in long-term financial planning is to choose between life insurance term and whole: which one makes sense? The correct decision would save your family, uphold wealth, and enhance future aspirations. The misfit is capable of sucking your budget several decades and doing so unnoticed. This manual simplifies all of this without using any jargon and makes sense in real life and thus does get you to make a decision.

Learning about the Search Intent Behind Term vs Whole Life Insurance.

The search purpose is mostly informational and has commercial undertones. Customers desire transparency to purchase. They are weighing prices, advantages, dangers, and financial profits in the long run. This guide will cover such an intention by explaining the concepts, providing comparisons as well as decision making.

Over latest post:Common Loan Mistakes That Cost Borrowers Thousands: 17 Shocking Errors to Avoid

What Is Life Insurance and Why It Is Important Financially.

Life insurance is a financial security. It can spread the risk of your family, trading it against your insurance company at a premium.

Basic Intention of Life Insurance.

- Replace lost income

- Final expenses and cover debts.

- Protect dependents

- Promote financial stability in the long run.

- The Fitting of Life Insurance into financial planning.

Life insurance is a supplement to savings, investments, retirement planning and estate plans. It is not only about death, it is about financial continuity.

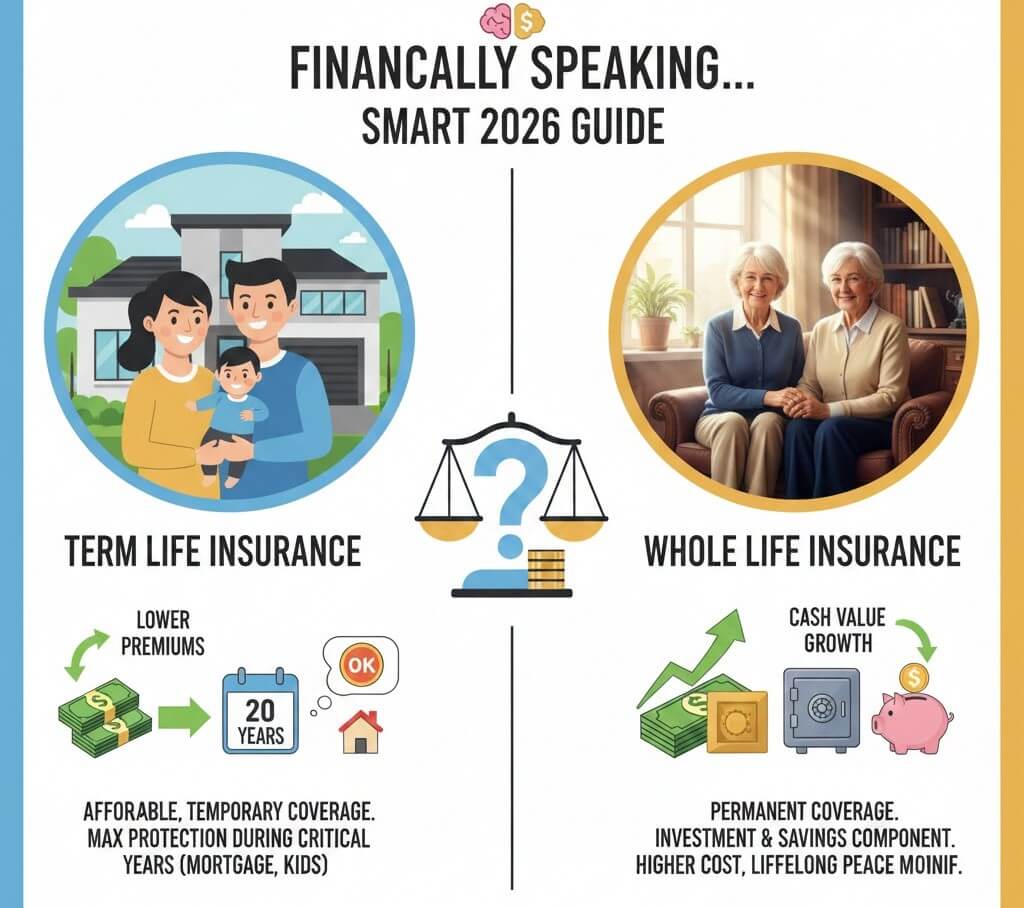

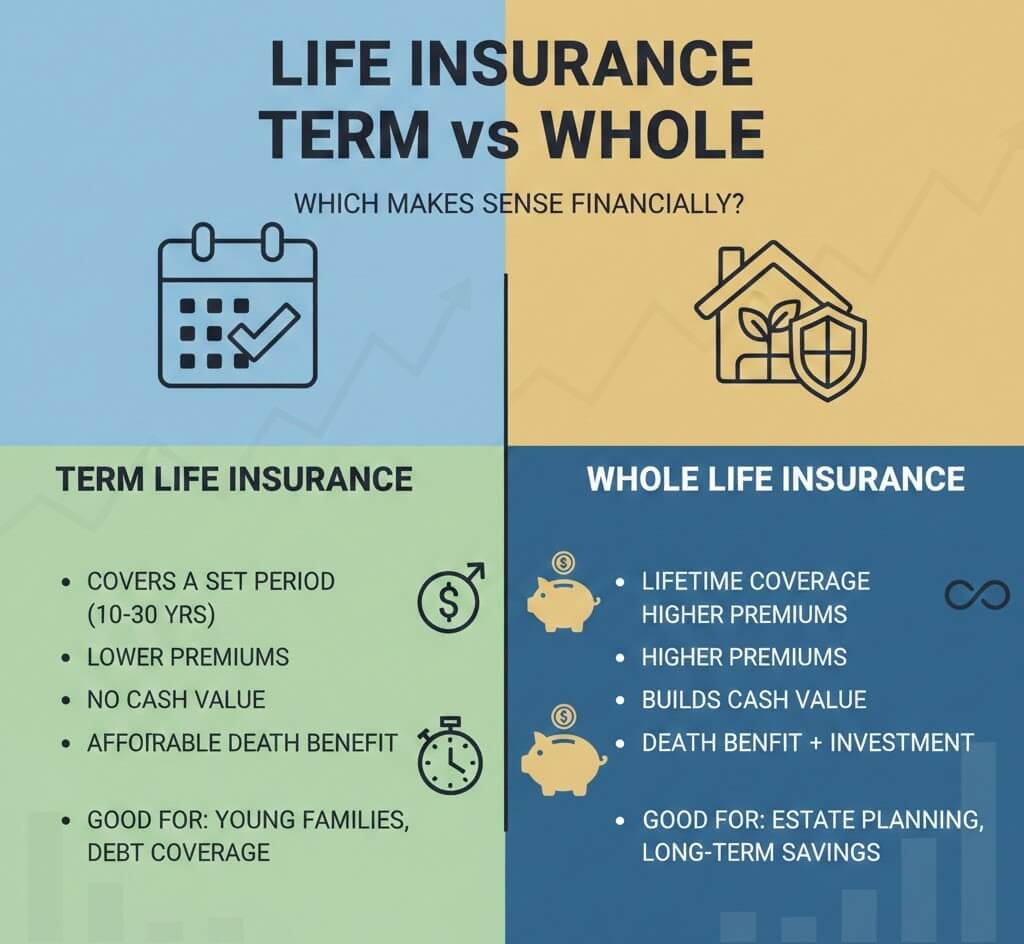

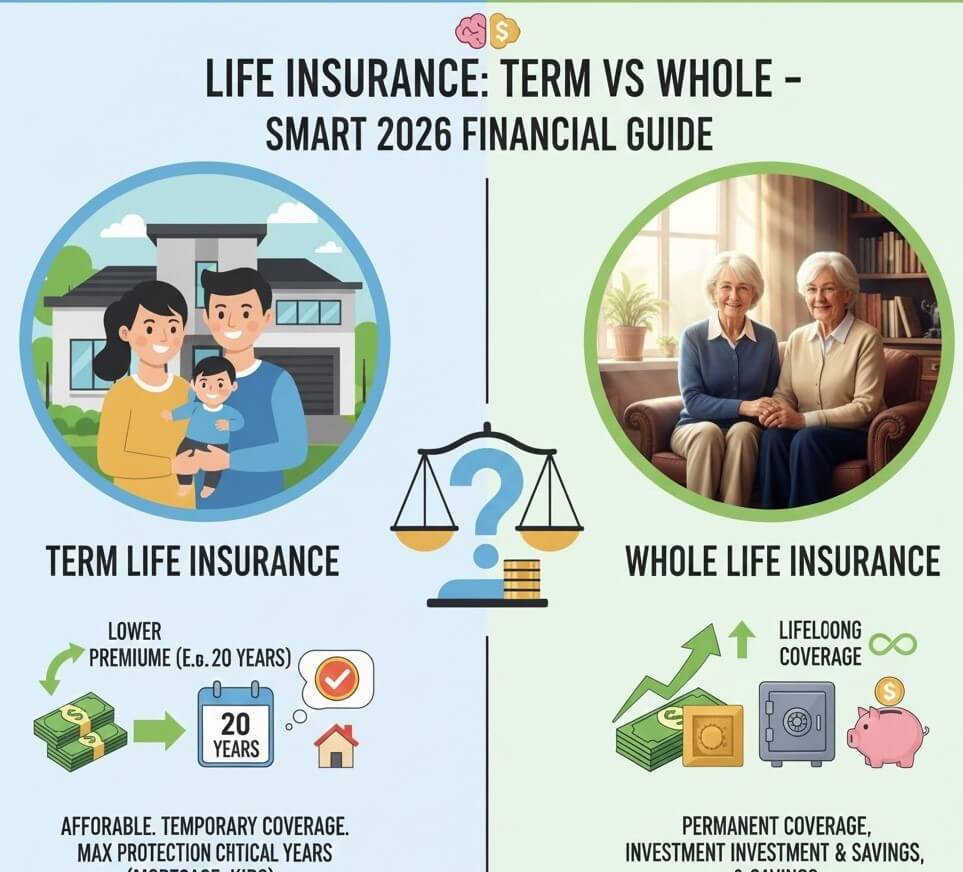

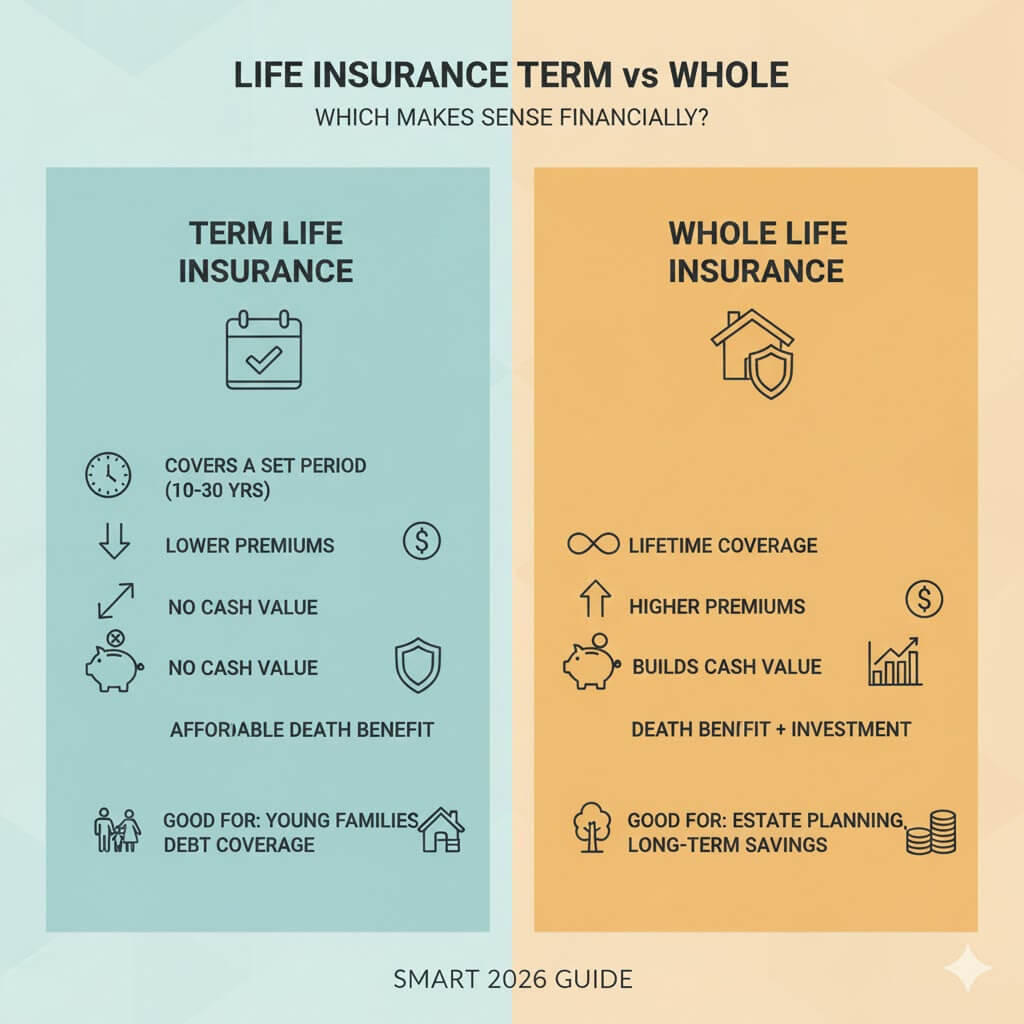

What Is Term Life Insurance?

Term life insurance is a kind of insurance that has a definite term to be covered, most of which are 10, 20, or 30 years.

Term life insurance operates in the following way.

You pay a fixed premium. In the event of your death during the term, then there is a death benefit to beneficiaries. Unless renewed, coverage ceases at expiry of the term.

Pivotal Advantages of Term Life Insurance.

Much decreased premiums.

- Simple and transparent

- Perfect as a substitute of income.

- Simple to find parallels to life stage coverage.

The Probable Cons of Term Life Insurance

- No cash value

- Coverage expires

- Renewal costs rise with age

Over latest post:What Lenders Look for Before Approving a Loan: 17 Proven Factors That Decide Approval

What Is Whole Life Insurance?

Whole life insurance is permanent and is a life time coverage provided you pay premiums.

The operation of Whole Life Insurance

Premiums remain fixed. A portion of the payment accumulates cash value which grows tax-deferred.

The major advantages of Whole Life Insurance

- Lifetime protection

- Cash value accumulation

- Predictable premiums

- Estate planning advantages

Possible Disadvantages to Whole Life Insurance

- High premiums

- Lower investment returns

- Less flexibility

Life Insurance Term vs Whole: Cost Comparison

Cost is the biggest deciding factor in life insurance term vs whole: which makes sense financially?

| Policy Type | Monthly Cost (Age 35) | $500,000 Coverage |

|---|---|---|

| Term (20-year) | $30–$45 | Yes |

| Whole Life | $400–$600 | Yes |

Term life allows higher coverage at lower cost. Whole life demands long-term commitment.

Over latest post:How to Increase Your Credit Score Fast Legit Methods OnlyProven 9-Step System That Works

Life Insurance term/whole Investment and Cash Value analysis

There is a savings aspect of whole life. Nonetheless, the returns are modest.

- Average whole life returns: 2–4%

- Long surrender periods

- Index investing vs opportunity cost.

There are numerous financial planners who recommend the purchase of the term and the difference and invest in diversified portfolios.

Term vs Whole: Flexibility and Control Life Insurance.

Term life provides flexibility. Coverage can be changed with changes in life. Whole life locks you in.

- Term makes an adjustment to mortgages, children, changes of career.

- Whole life suits are long term and predictable.

Whole vs Life Insurance Term: Taxes.

The two policies provide tax-free death benefits.

Whole life advantages:

- Tax-deferred cash growth

- Tax-advantaged loans

Outside authority on tax regulations:

IRS Life Insurance Tax Guidelines (irs.gov).

Which Life Insurance type is better: Term or Whole Life

The Best Option to Young Families.

Term life. The coverage will be very high, and the cost will be low, and maximum protection will be provided when earnings are in full bloom.

Better Alternative to Higher Income Earners.

Whole life can be used on top of estate planning once the tax shelters are filled.

Most Ideal with regards to Estate Planning.

Whole life is liquidity in the form of estate taxes and transfer of wealth.

Real life situations and financial illustration.

- Scenario 1: Parent is a 30-year-old and he/she selects term and invests in savings. Net worth grows faster.

- Scenario 2: Buy-sell agreement and tax planning A business owner opts to use whole life.

- The actual results are measured in terms of discipline, income stability, and goals.

Term and Whole Life Insurance Total Myths

- Whole life is never a good investment – Not always.

- Protection has value “Term life is throwing money away”

- “Savings account = cash value” – Not so.

Over latest post:Credit Score vs Credit Report: What Banks Actually Check – Powerful Guide 7

Which Insurance should you choose? Decision between Term and Whole Life Insurance.

Ask these questions:

- Who depends on your income?

- What is the estimated duration of protection required?

- Is flexibility important?

- Do you maximize other investments in the first place?

Frequently Asked Questions

Is whole life better than term life insurance?

For most families, yes. It is cost effective and adaptable.

Is it possible to convert term life into whole life?

There are numerous policies where conversion can be done without medical checkups.

Does whole life insurance increase wealth?

Slowly. More a question of stability than growth.

What is the case when term life runs out?

Cover ceases except in cases of renewal or conversion.

Is whole life insurance tax free?

Death benefits are usually tax free. Appreciation of cash values is tax-deferred.

What is the policy suggested by financial advisors?

The majority of them suggest term life and investing in other places.

Final Verdict: Life Insurance Term Vs Whole.

In asking life insurance term vs whole: which makes sense financially? the answer will be based on goals, income and discipline. Term life is a winner in the area of affordability and effectiveness. Whole life is appropriate to niche strategies, preservation of wealth and estate planning.