Introduction

Learning How Personal Loan Interest Rates in the USA are computed is the key to making wise financial choices on the part of a borrower. Interest rate will dictate what will be paid back throughout the loan life and even a slight variation will save or cost you thousands. This paper reveals all of that, what the interest rate actually is, how it is computed by lenders, what affects it, and how you can negotiate improved conditions.

Interest rates are not on a piece of paper but it embodies credit risk, market trends and consumer financial health. We will go through the formula of simple and compound interest, contrast between APR and interest rate as well as provide real life examples to decipher math so that you can approach lenders with confidence.

What is an Interest Rate?

Interest rate refers to the amount of money charged to borrow money given as a percentage of the borrowed sum. This is because when you borrow a personal loan, the financial institution will charge you an interest on the service of giving you money now instead of giving you money later.

Key Definitions

- Principal – Amount you borrow

- Interest Rate- Percentage cost of borrowing per year.

- APR (Annual Percentage Rate) – It consists of interest and fees.

- Simple Interest – Interested on principal alone.

- Compound Interest- Interest calculated on the principal and accrued interest.

To get the difference simply imagine a 10,000 dollar loan: a 10-percent per-year simple interest charge implies that the loan will receive a 1,000 dollars of interest annually on the loan principal.

Over latest post:The credit scores work in the USA (2026 Guide)

Personal Loans in the USA: An Overview

Personal loans are unsecured loans which are used by the borrowers in numerous uses that include debt consolidation, medical bills, travel, and home improvements among others. The banks, credit unions, and online lenders offer these loans in the U.S. Since they are not secured, the interest rates tend to be higher than the secured loans such as mortgage loans.

The U.S. lenders are supposed to report the APR which gives clarity on the overall cost of borrowing. This allows you to compare lenders fairly- not just admire the rate of interest advertised.

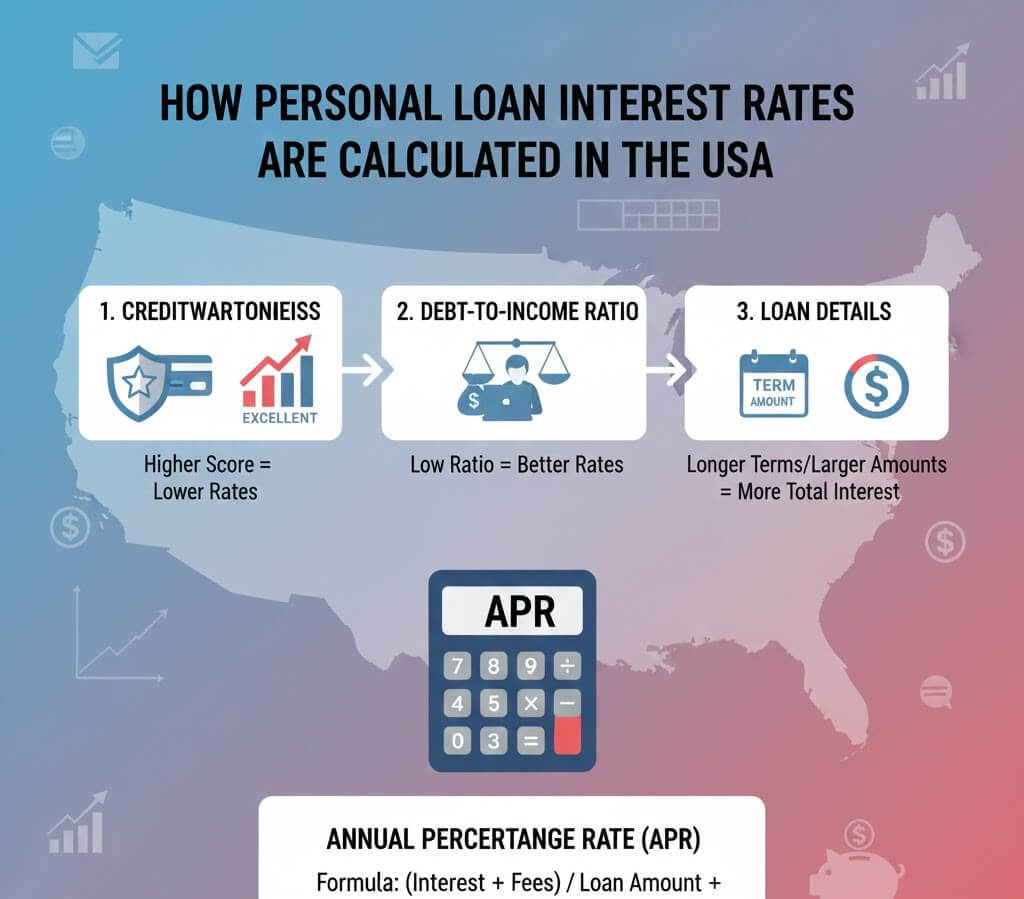

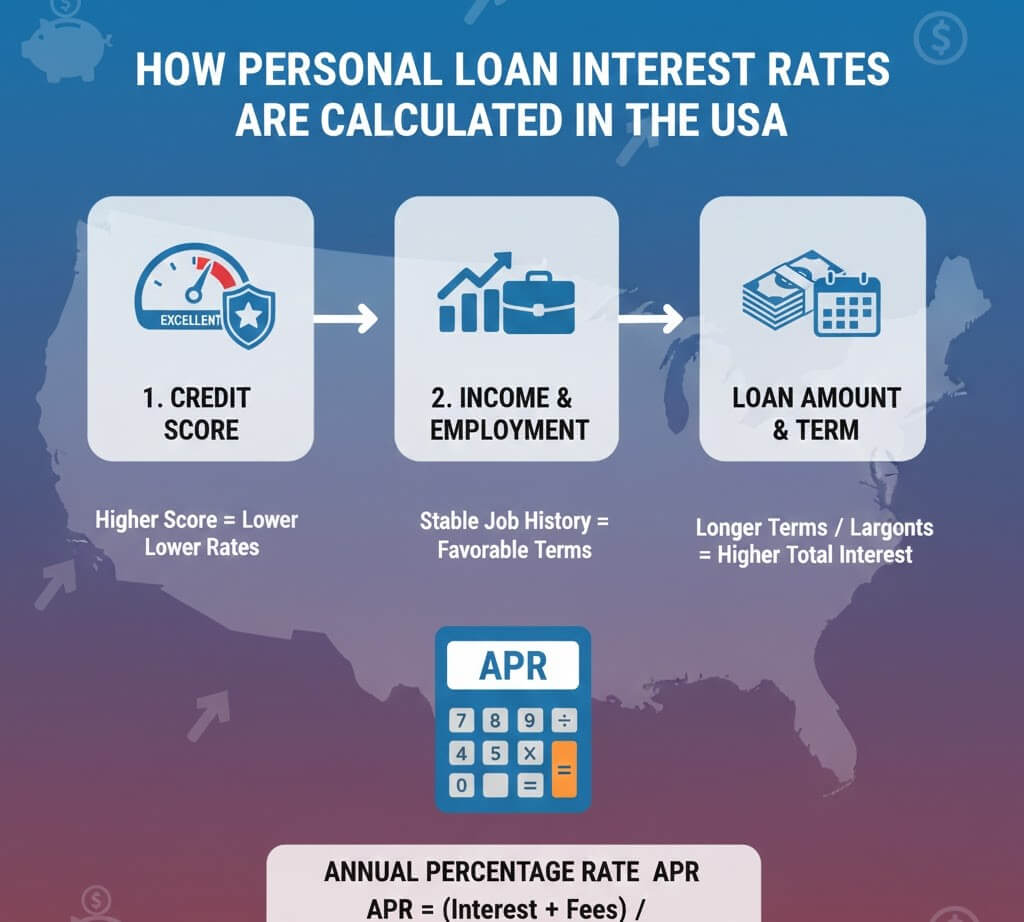

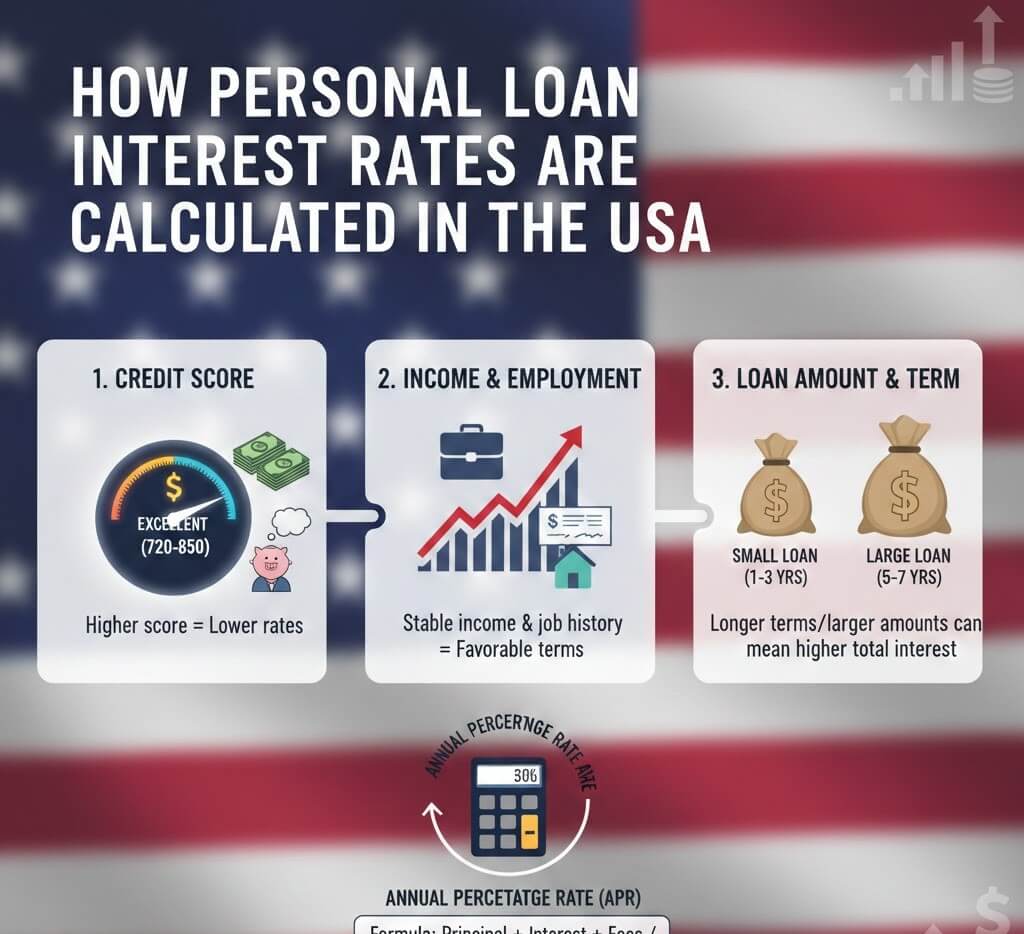

What Influences Personal Loan Interest Rates?

There are no arbitrary interest rates. There are numerous criteria that lenders apply in determining risk, and how expensive to lend to you.

Major Factors

- Credit Score- The higher the score the lower the rate.

- Income and Job Stability- Foresees repayment capacity.

- Debt-to-Income Ratio (DTI) – Indicates financial burden.

- Loan Amount and Term- The longer the term, the higher the rate.

- Economic Conditions – The interest rates on the market determine the interest rate charged by the lenders.

All these are contributors to a risk profile. Lenders desire a trade off; to reward low-risk borrowers with better rates and to insure themselves against any possible defaults.

Lender Calculations: How Interest Rates Are Set

Lenders start with a base rate influenced by broader economic benchmarks such as the prime rate, which the Federal Reserve indirectly shapes through monetary policy.

Basic Formula for Interest

For simple interest, the formula is:

Interest = Principal × Rate × Time

If you borrow $10,000 at 12% for 3 years:

$10,000 × 0.12 × 3 = $3,600 total interest

But most personal loans use amortization, where monthly payments pay both principal and interest.

Monthly Payment Formula

Lenders use the amortization formula:

M=P×(1+r)n−1r(1+r)n

Where:

- M = monthly payment

- P = principal

- r = monthly interest rate (annual rate ÷ 12)

- n = number of payments

This guarantees every monthly payment is an equal amount, but a percentage will be sent to interest where the amount will reduce.

APR vs Interest Rate: Why It Matters

APR indicates all the cost of borrowing, such as origination fees. The interest rate merely demonstrates the fee of the lender to the loan itself.

- Interest Rate -Expense of lending principal.

- APR -interest rate with fees.

To compare shopping, you should always use APR. Two lenders could both be advertising 10, but when one of them has greater fees, the APR may be a lot more.

Fixed vs Variable Rates

- Fixed Rate: The fixed rate is maintained throughout the entire life of the loan. Payments that are predictable aid in budgeting.

- Variable rate: varies with the market. Can start lower but increase.

The majority of personal loans are fixed rate loans. Such variable rates are more prevalent in home equity lines of credit or credit cards.

The impact of Loan Term on the cost of interest.

Longer terms soften the amount of monthly payment and make the overall interest payment higher. Shorter terms are more expensive to tap on per month yet less in total interests.

Example:

| Term | Monthly Payment | Total Interest |

|---|---|---|

| 3 years | $332 | $1,952 |

| 5 years | $212 | $2,735 |

This shows why understanding term impact matters.

Credit Score’s Role

A credit score is one of the best indicators of the interest rate you would get. Typical credit tiers:

- Excellent (750+) – Best rates

- Good (700-749) – Competitive rates

- Fair (650-699) – Mid-range rates

- Poor (<650) – High rates or denial

It is better to raise your score before you can apply.

Debt-to-Income Ratio (DTI)

- DTI = Monthly debt payments/ Gross monthly income.

- A low DTI informs the lenders that you have space to cover new payments, thus enhancing your rate.

Economic Standards and Market Conditions.

Rates are pegged by lenders to broader markets. The Federal reserve has an impact on the prime rate, which influences the pricing of interest charged on personal and business loans. In the tight economy or inflation, the rates are likely to go up.

The Federal Reserve provides data on the official prime rate on its data page.

How you can Reduce Your Personal Loan Interest.

- Ease credit score prior to application.

- Choose a shorter loan term

- Reduce existing debts

- Apply with a co-signer

- Shop multiple lenders

It is possible that negotiation can work with good financials as well.

Misperceptions of the Personal Loan Interest.

- Guaranteed Lowest advertised rate. No — your rate is personalized.

- The same is considered by all lenders. Credit unions are also able to provide superior terms to those provided by banks.

- “Fees don’t matter.” Commissions affect APR and overall cost.

Actual Cases: Calculation of Interest Rates.

Scenario 1: Excellent Credit

Borrower: $15,000

Credit score: 780

Rate: 9% APR

Term: 4 years

Amortization and monthly payment depict lower expense than a borrower with a lower score.

Scenario 2: Fair Credit

Borrower: $15,000

Credit score: 640

Rate: 17% APR

Term: 4 years

Increased payments, and total interest paid – indicate effect of credit risk.

Frequently Asked Questions

How is the interest charged on personal loans computed in the USA?

Monthly, interest is computed according to your interest rate, term and value with the help of amortization formulas.

How much interest should be charged on a personal loan?

Good credit has in the middle to high single digits, whereas, poor credit moves to the double figures.

Does APR include fees?

Yes – APR consists of both interest and necessary charges and is more suitable to compare.

Is my loan rate vulnerable to market rates?

Yes – wider economic rates affect the starting base rate of the lenders.

Will an additional principal payment be of interest?

Yes – the additional payments made on principal decrease future interests.

Is it better to keep it fixed or variable rate?

The majority of personal loans are non-variable and provide predictability of payment.

Conclusion

Learning about the How Personal Loan Interest Rates are computed in the USA will enable you to shop better, bargain and save on the cost of taking loans. Interest rate is based on credit fitness, income, loan conditions, rates in the market and charges. You can get lower rates and save in the long-run by enhancing your credit, controlling your debts and shopping around lenders.

Pay attention to the total price, not only the price that is advertized, and employ such tools as APR to compare the lenders smartly. You can now go out there with the knowledge to deal with personal loans.