How Credit Scores Really Work in the USA (2026 Guide)

In America, everyday financial life is determined by credit scores. Whether it comes to mortgages or car loans, whether you rent an apartment or you pay insurance, whether it amounts to dollars saved or dollars spent, your score is silently considered to make or save you money. In this How Credit Scores Really Work in the USA (2026 Guide), the system is disaggregated in straightforward words. No hype. No myths. And how exactly it will work in 2026 and how to make it work to your benefit.

Learning about the Credit Scores in the United States.

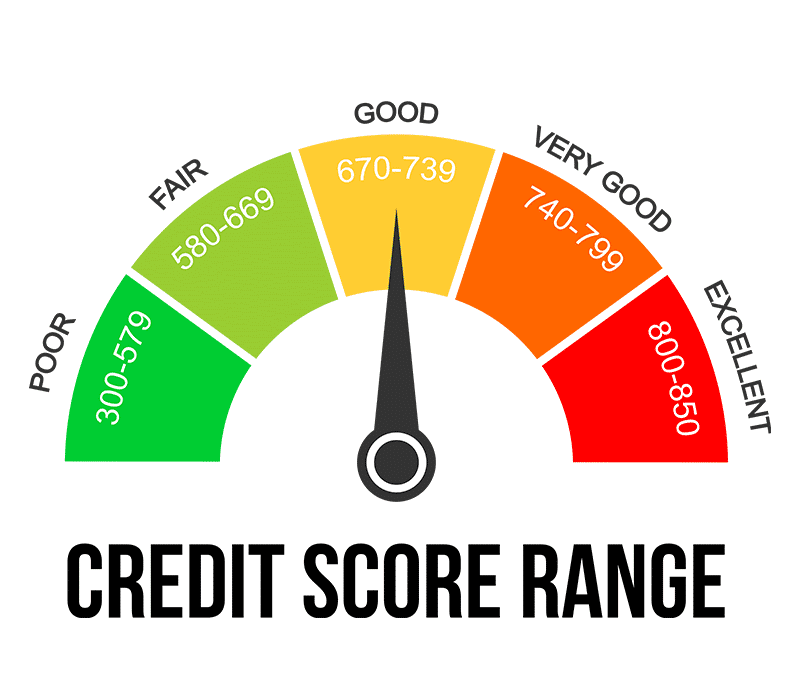

A credit score is a mathematical summary of your financial report on managing money owed. The majority of credit scores in the U.S. are between 300 and 850 where the higher the score, the less risky it is to the lending institution.

The Real Measure of a Credit Score.

In contrast to what many people think, credit scores are not an indicator of income, net worth, and savings. They track behavior:

- Do you pay bills on time?

- How much credit do you use?

- How many years have you been in charge of credit?

- You take out new accounts very often?

The system is predictive. It looks back in order to determine future risk.

The More Importance of Credit Scores In 2026.

- In 2026, credit ratings will have greater influence than borrowing:

- Mortgage and auto interest rates.

- Approval of rentals and deposits.

- The price of insurance in most states.

- Terms of utility and phone services.

A single point difference in the score can translate into a thousand dollar difference in the lifetime of the loan.

Explanation of the Credit Scoring Models.

FICO Score vs VantageScore

Two main scoring systems dominate the U.S. market:

| Model | Primary Users | Notes |

|---|---|---|

| FICO | Banks, mortgage lenders | Used in ~90% of lending decisions |

| VantageScore | Credit apps, fintechs | More forgiving for short histories |

Both use similar data but apply different math.

The reason you do not have one credit score.

You have several scores due to:

- It has three credit bureaus ( Experian, Equifax, and TransUnion ).

- The different bureaus might contain various data.

- There are various scoring models.

That’s normal. The score selected by lenders corresponds to the risk model.

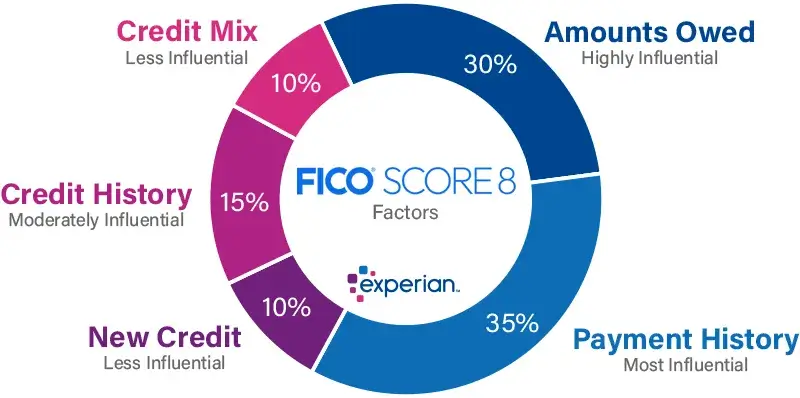

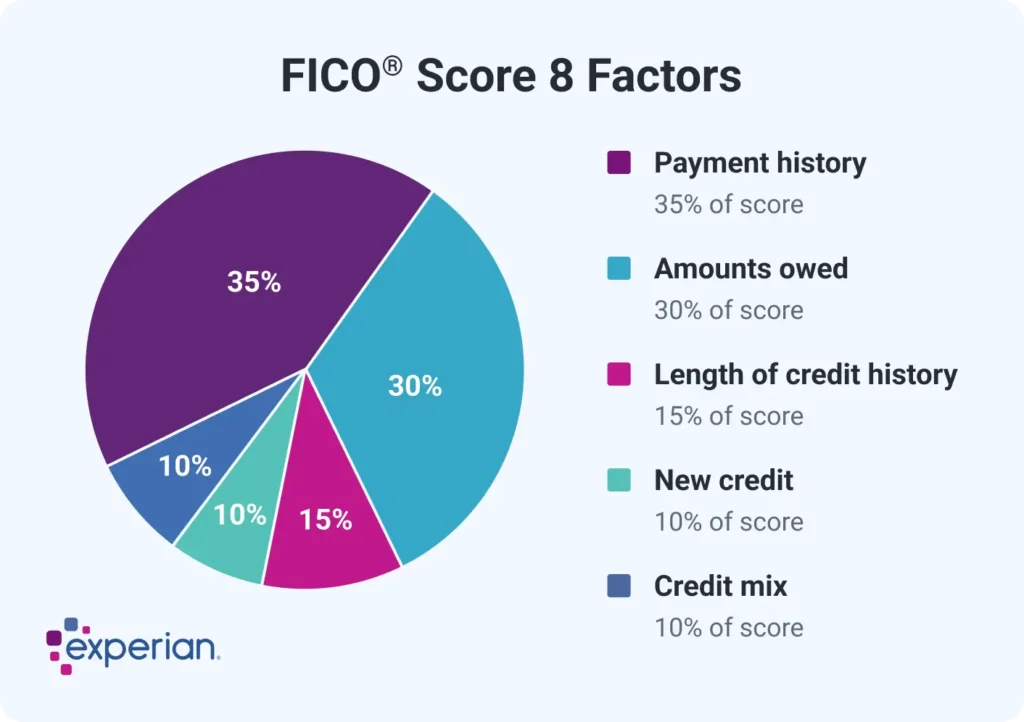

The Five Things to Know to Build Your Credit Score.

Payment History (35%)

Most weight is placed on payment history. Delay in paying can be very disastrous.

What hurts most

- 30+ day late payments

- Collections

- Charge-offs

Practical experience: A poor rating can be lowered by 80 or more as a result of just one late period.

Credit Utilization (30%)

Utilization is a measure of the amount of your available credit that you are utilizing.

- Healthy benchmarks

- Under 30%: acceptable

- Under 10%: ideal

Huge balances are warning signs–even when you pay in full every month.

Length of Credit History (15%)

- Time matters. The reason behind older accounts is that it exhibits stability over time.

- Savvy: Have your eldest credit card which is not charged open.

Credit Mix (10%)

- The combination of types of credit exhibits elasticity:

- Revolving credit (cards)

- Installment loans (car, student, mortgage)

- You need not have all of them, but serious use.

New Credit & Inquiries (10%)

- Hard inquiries reduce scores marginally over a period of one year.

- Tip: Shopping of a loan within a short timeframe is typically considered as having one inquiry.

What Will Change the Credit Scores in 2026.

Medical Debt Reporting

Medical collections with payment are cleared quicker. Little balances remaining unpaid have less of an impact on the scores.

Buy Now, Pay Later (BNPL)

There are those BNPL providers that are activity reporting. On-time payments can help. Missed payments can hurt.

Rent and Utility Payments

Additional reporting choices will enable renters and first-time borrowers to develop credit with non-loans.

Myths of Credit Score that Continue to Damage people.

- Billing credit reduces your score – not true.

- You need to have a balance to establish a credit – fake.

- It helps to close cards – normally false.

- Income has an impact on your score – false.

- The assumption of these myths causes unnecessary harm.

How Lenders Actually Use Your Credit Score

Borrowers are categorized according to their level by lenders:

| Score Range | Classification |

|---|---|

| 300–579 | Poor |

| 580–669 | Fair |

| 670–739 | Good |

| 740–799 | Very Good |

| 800–850 | Excellent |

The higher the levels, the better the rates, higher the limits and quicker approvals.

It is necessary to define how to improve your credit score in 2026 (Step-by-Step).

Draw end-of-run reports of the three bureaus.

- Dispute errors immediately

- Pay cards below 10% utilization

- Request credit limit advancements.

- Avoid closing old accounts

- Include rent or utility reporting.

- Borrow new credit, but not frequently.

Result based on experience: The vast majority of the population also records improvements in the score within 30-60 days.

Credit Reports and Credit Scores.

| Credit Report | Credit Score |

|---|---|

| Full payment history | Risk snapshot |

| Updated continuously | Calculated instantly |

| Can contain errors | Reflects report data |

Fix reports first. Automatic follow-up scores.

Credit Surveillance The Smart Way.

Free monitoring software notifies you of:

- New accounts

- Balance changes

- Missed payments

The early detection helps to avoid the long-term damage.

Ask Ubuntu: How credit scores actually work in the USA (2026 Guide)?

What are the frequency of credit scores updating?

Whenever lenders report new data, which is normally on a monthly basis.

How can you boost a credit score (in the shortest time possible)?

Decreased credit card balances of less than 10% utilization.

Is a 700 credit score good in 2026?

Yes. In most cases, it competes on its own rates.

What is the length of time to hold up late payments on a report?

A maximum of seven years, less severely with time.

Are there any benefits of paying off debt that leave it off reports?

No. Paid accounts are not deleted but are in positive status.

Can rent really build credit?

Yes, when payment is reported by certified services.

Conclusion

The article How Credit Scores Really Work in the USA (2026 Guide) demonstrates one thing: the system is not a chance and does not work against people, it is organized. You can be able to work the rules when you know the rules. Scoring in credit favors stability, forbearance, and risk aversion. Control those and your score is not a mystery, but a strong financial asset.