Learning About Search Intent and the Importance of This Topic

The key purpose of Credit Score vs Credit Report: What Banks Actually Check is informative and has a high level of commercial interests. Individuals who have entered this query are most likely in the process of applying to take a loan, credit card, or mortgage. They want clarity, not jargon. They are wondering: What banks really consider- and how can I have any effect?

This guide is more than what is on the surface because it combines the lender practices, real-life lending experience, and credible sources like Equifax and Experian. It is created to assist the user in making wiser financial decisions.

What is a credit score and why is it important that banks took an interest in it?

A credit score is a number that is used to summarize your credit risk. Banks will be fond of it since it is fast, standardized, and predictive.

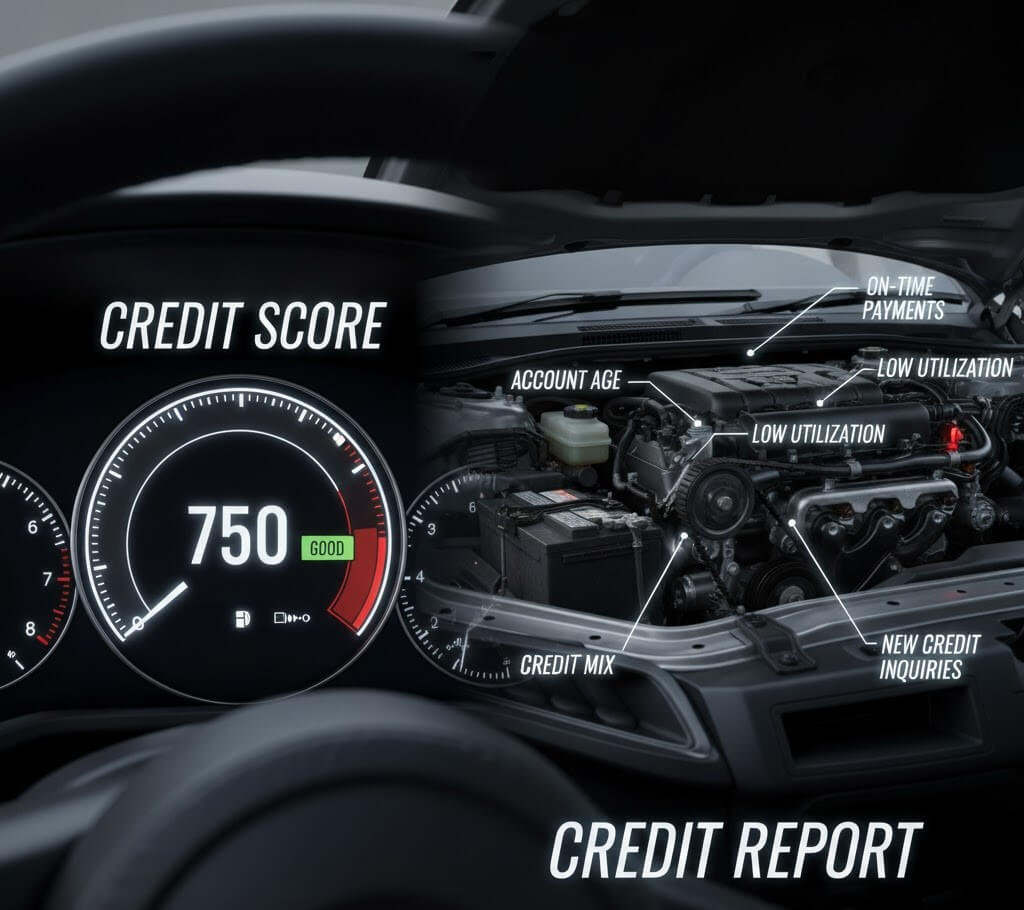

The Method of Calculating Credit Scores

The FICO or other scoring models are used by most lenders. Formulas differ, but the following factors are normally applicable:

Payment history ([?]35%) – Are you a paid up person?

- Use of credit ([?]30%) – What percentage of your available credit do you use?

- Credit history length ([?]15%)

- Credit mix ([?]10%)

- New credit inquiries ([?]10%)

The score is frequently used as a filter by banks. When it is lower than their cutoff, the application will never get to a human.

Score Ranges and What they are an Indicator of

- 300-579: High risk

- 580-669: Fair

- 670-739: Good

- 740-799: Very good

- 800-850: Excellent

The higher the score, the less interesting the rates and the quicker approvals.

Lending Decision Real-World Situation

Loan officers in retail banking get two applicants with the same incomes most of the time. The one that has a score of 760 is immediately approved. The other that is 640 causes additional checks–or rejection. That’s the power of a score.

Over latest post:Best Credit Score Range for Personal Loans and Credit Cards Proven Guide (2025)

The Full Financial Story of credit Report Explained

When the headline is a credit score, then that credit report is the whole article.

What is on a Credit Report

An average credit report contains:

Name, address, phone number, etc.

- Credit open and closed accounts.

- History of payment on every account.

- Credit limits and balances

- Hard and soft inquiries

- Public records (where there are any)

According to the authoritative sources such as Equifax, lenders consult the report to clean up the accuracy behind the score (external reference: Equifax education resources).

Mistakes, Conflicts, and their effect

Errors are made- duplicate accounts, out of date balances or false late payments. Approval odds can be decreased by even a single mistake. Senior borrowers are used to checking reports prior to application and challenge problems at an early stage.

Reading credit reports by Lenders

Banks do not read reports directly: numbers are not all they scan:

- Recent missed payments

- Rising balances

- Too many new accounts

- Stability over time

- Here it is the context that counts.

Over latest post:Why Credit Card Utilization Matters More Than You Think: 15 Powerful Insights

Credit Score vs Credit Report: Key Differences Side-by-Side

Understanding Credit Score vs Credit Report: What Banks Actually Check requires seeing how they work together.

Quick Comparison Table

| Feature | Credit Score | Credit Report |

|---|---|---|

| Format | 3-digit number | Multi-page document |

| Purpose | Predict risk quickly | Show detailed history |

| Used for | Fast decisions | Manual review |

| Can change fast | Yes | Slower |

| Includes context | No | Yes |

Banks don’t choose one over the other—they use both.

The Real Checks Banks Do on Your Application

This is the reality that lenders hardly articulate.

Automated systems vs. Human Review

- Automated checks your score during underwriting.

- Your credit report is scanned by systems in case you pass.

- In case of large loans, all is reviewed by a human underwriter.

That is why applicants who have the same score may receive unequal results.

Your credit data is also compared to that of banks:

- Income stability

- Debt-to-income ratio

- Employment history

The credit information is the gateway and the financial stability is the continuum.

How to Improve What Banks See

You do not have to have tricks, just consistency.

Short-Term Fixes

- Balance pay down less than 30% usage.

- Fix accurate mistakes in your credit report.

- New hard inquiries before applying should be avoided.

Long-term and credit health plans

- Keep old accounts open

- Keep credit to a minimum but frequent.

- Always pay bills at the right time- no exceptions.

These habits enhance your score and report which is what the banks desire.

Over latest post:Secured vs Unsecured Loans: Which One Costs You More? | 7 Powerful Cost Truths Revealed

The Myths that Borrowers continue to believe in

Myth: “It does not count but my credit score.

Fact: Reports are as important as well.

Myth: “Checking my report brings down my score.

Truth: It doesn’t.

Myth: “Better income cures bad credit.

Fact: Income is an assist, but credit history prevails.

Frequently asked questions (FAQs)

- Are credit score or credit report checked by the banks?

They tend to have a glance at the credit score first and then the credit report.

- Is a low score compensated by a good credit report?

Sometimes. Powerful history and explanations could be used in manual reviews.

- How frequently would I monitor my credit report?

Once a year or three days before major applications.

- What does it mean by seeing a different score among lenders?

There are variations in different scoring models and report data.

- Would banks view my entire credit history?

Yes, generally 7 10 years based on the item.

- Will one missed payment be a deal killer?

Not always, but the late payments in the recent past are a cause of concern.

Over latest post:Auto Insurance Explained: What Coverage Do You Actually Need? | Ultimate 2025 Guide

Conclusion: The End of the Road on Credit Decisions.

In the case of Credit Score vs Credit Report: What Banks Actually Check, there is one simple answer to the question: both are important and they complement each other. Your score opens doors. Your report tells me whether you have the right to walk through them or not.

You will need to learn how lenders operate in their mindset, anticipate it, and you will be at the helm, less stressed, and more likely to be approved. True financial confidence.