Ideal Personal Loan and credit card credit score

You are not alone in questioning about the Best Credit Score Range when loaning personal money and using credit cards. Millions of borrowers are looking to this very question before they seek financing- and with reason. Your credit rating is a direct determinant of the approval chances, interest rates, limit, and even trustworthiness of the lender. This all-encompassing guide will give you the precise credit score ranges that will open the best deals in the personal loans industry and elite credit card deals, as well as how to strategically boost your score.

Over latest post:The credit scores work in the USA (2026 Guide)

Credit Scores: What to know in a Minute.

What Is a Credit Score?

A credit score refers to a three-digit number; usually between 300-850 indicating how well you pay your debts. It is determined based on the information about your credit reports, which encompassed payment history, credit utilization, length of credit history, credit mix, and recent inquiries.

📌 Expert Insight: Experian believes that the number of payments you make is a 35-percent component of your total score, which is why it is also the most influential factor.

The Importance of Credit Scores to Loans and Cards.

Your score is used to foresee risk by the lenders. The better the score, the better the lenders are convinced that they will receive the repayment. This directly affects:

- Approval likelihood

- Interest rates

- Credit limits

- Loan terms

Over latest post:How Personal Loan Interest Rates Are Calculated in the USA 2026

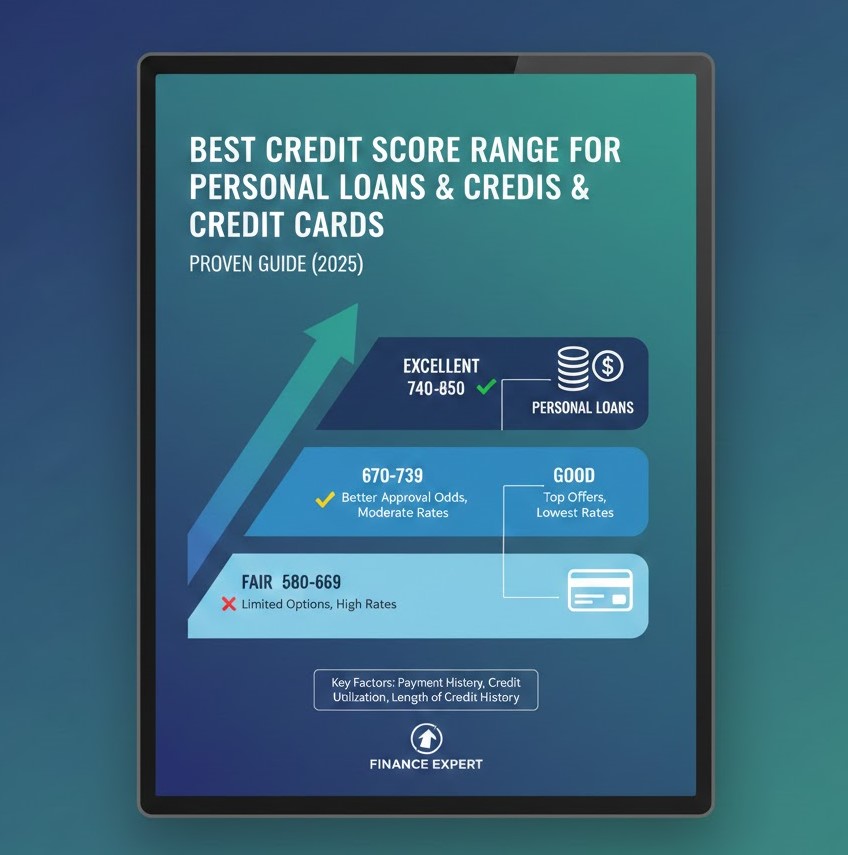

Credit Score Ranges Explanations

The understanding of how scores are categorized is required before determining the Best Credit Score Range to use when taking a loan on a personal basis and/or when taking out a credit card.

Poor Credit Score Range (300–579)

- High risk for lenders

- Limited approval options

- Increased interest rates and charges.

Fair Credit Score Range (580–669)

- Simple loan and card qualification.

- Moderate interest rates

- Frequently needs a check of income.

Good Credit Score Range (670–739)

- Strong approval chances

- Competitive interest rates

- Access to superior rewards cards.

Very Good Credit Score Range (740–799)

- Preferred borrower status

- Low interest rates

- Premium credit card offers

Outstanding Credit Score (800 to 850)

- Optimal terms and rates.

- High credit limits

- Exclusive perks and bonuses

Over latest post:How Health Insurance Really Works in the USA 2026

Optimal Personal Loan and Credit Card Best Credit Score.

Perfect Personal Loan Score Range.

The Optimal Personal Loans/ Credit Card Best Credit Score begins at 670 but ideal terms are usually at 720 and onwards.

The Breakdown of the score on personal loans:

- 670-699: This is probably good, mediocre rates.

- 700–739: Low interest rates

- 740 +: Favourable loan conditions, optimum loan limits.

Bankers and credit unions are very much encouraged on borrowers within this bracket.

Credit card Ideal Score Range.

In the case of credit cards, particularly rewards cards as well as travel cards, the sweet spot is 700-750+.

- 670–699: Basic cards, limited rewards

- 700–739: Cashback and entry rewards

- 740+: Premium and luxury cards, travel.

The Evaluation of the Credit Scores by Lenders.

Role of FICO vs VantageScore

The majority of lenders make use of FICO scores, and some fintech lenders depend on VantageScore. Both models put into consideration similar factors although FICO is the industry standard.

Other Non-Credit Score Factors

Lenders also consider: even in the Best Credit Score Range under Personal Loans and Credit Cards:

- Income stability

- Debt-to-income ratio

- Employment history

- Outstanding credit commitments.

Over latest post:How a Bad Credit Score Affects Loan Approval – 17 Powerful Facts Lenders Don’t Tell You

Interest Rates by Credit Score Range

| Credit Score | Personal Loan APR | Credit Card APR |

|---|---|---|

| 580–669 | 18%–36% | 22%–29% |

| 670–699 | 10%–18% | 18%–24% |

| 700–739 | 7%–12% | 15%–20% |

| 740+ | 5%–9% | 12%–17% |

The Strategic Way to Improve Your Credit Score.

Suggestions on Short-Term Credit Improvement.

- Less than 30% pay balance utilization.

- Avoid new credit inquiries

- Pay all bills on time

Strategies in Long-Term Credit Building.

- Keep old accounts open

- Diversify credit mix

- Check credit reports on a regular basis.

Myths of Common Credit Score Debunked

- The process of checking your credit damages your credit score.

- A balance has to be carried to establish credit.

- A high income represents a high credit score.

- All false. Sustainable consumption is much more important than wealth.

Credits Score Requirement by the loan type.

Secured vs Unsecured Loans

Collateral is better in secured loans. Unsecured loans require greater scores.

Rewards Credit Cards and Basic Cards.

Good to Excellent credit score is normally required in the reward cards.

On-the-job Knowledge and Information

Borrowers in the Best Credit Score Range to get Personal Loans and Credit Cards will always make thousands of dollars in savings in the form of interest alone according to the financial advisors. The score of 740 or more can save up to 50 percent of APRs relative to fair credit borrowers.

Frequently Asked Questions frequently asked questions (FAQs).

What is the lowest credit score on personal loans?

The lowest lenders will need 600 and the best would be 670 and above.

What is the credit score required to be on premium credit cards?

Usually 720 or higher.

Will I be granted with a reasonable credit score?

Yes, but assume increased interest rates.

How quickly can I raise my credit score?

With consistent efforts, noticeable improvements would be possible within 3-6 months.

Do lenders dislike credit score or income more?

The latter is important, though credit score may come first.

Is 700 a good credit score?

Yes-700 falls in the Best Credit Score Range of Personal Loans and Credit Cards.

Conclusion

Knowing the Best Credit Score Range on Personal Loans and Credit Cards will help you borrow better, save less and have access to premium financial services. A score of 700 and above will provide competitive rates, terms, and confidence by the lender. Through titanic training and premeditation, it is quite possible to achieve–and stay within–this sphere.