Secured and Unsecured Loans: Which One Is More Costly To you?

In the process of reasoning about Secured vs Unsecured Loans: Which One Costs You More, what consumers tend to be asking themselves is this: How much would this loan really cost me in the long run? The suggested purpose is plainly informational, with a commercial interest in it, and it is just what we shall deal with here–in a plain, honest and straightforward manner.

Within a few minutes of reading, you will realize the impact that the collateral, interest rates, fees, risk, and borrower profile have on overall cost of a loan. More to the point, you will have an idea of which type of loan is viable in your real life scenario rather than in the paper.

Understanding Secured vs Unsecured Loans Basics

We must first get a common ground of understanding how every type of loan functions before we compare costs.

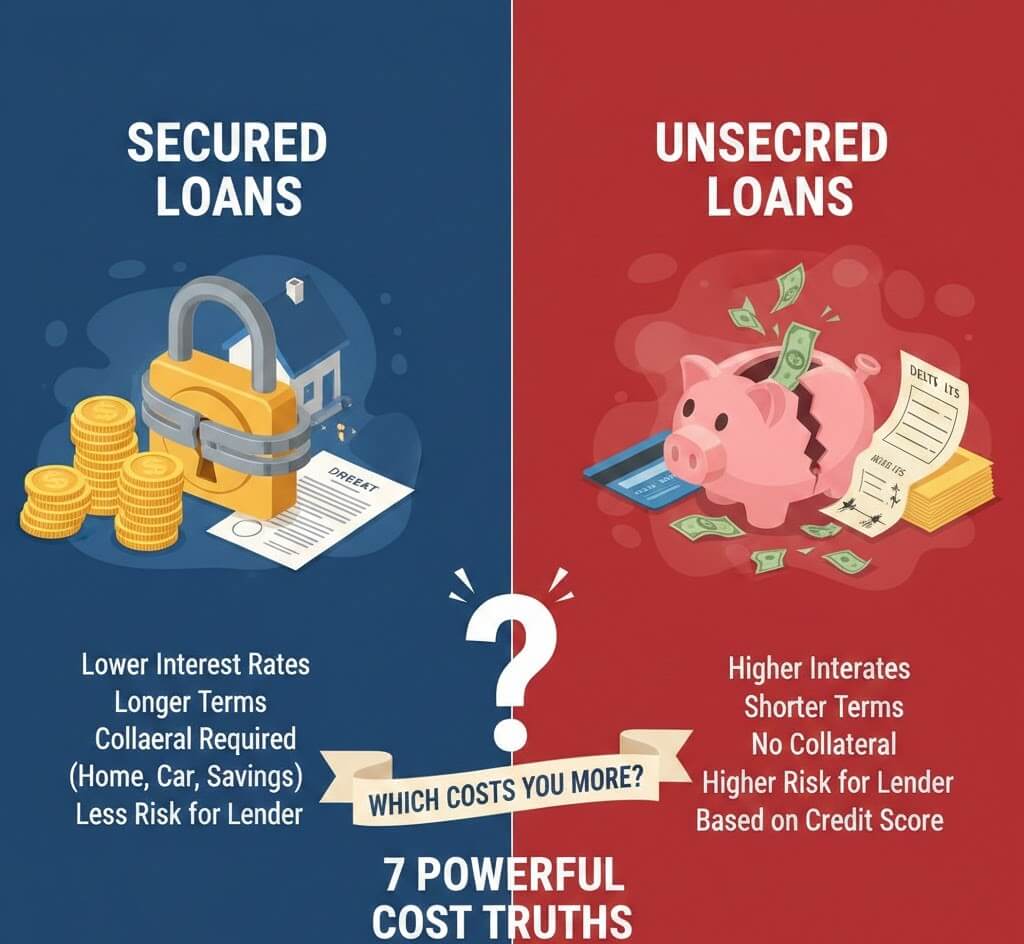

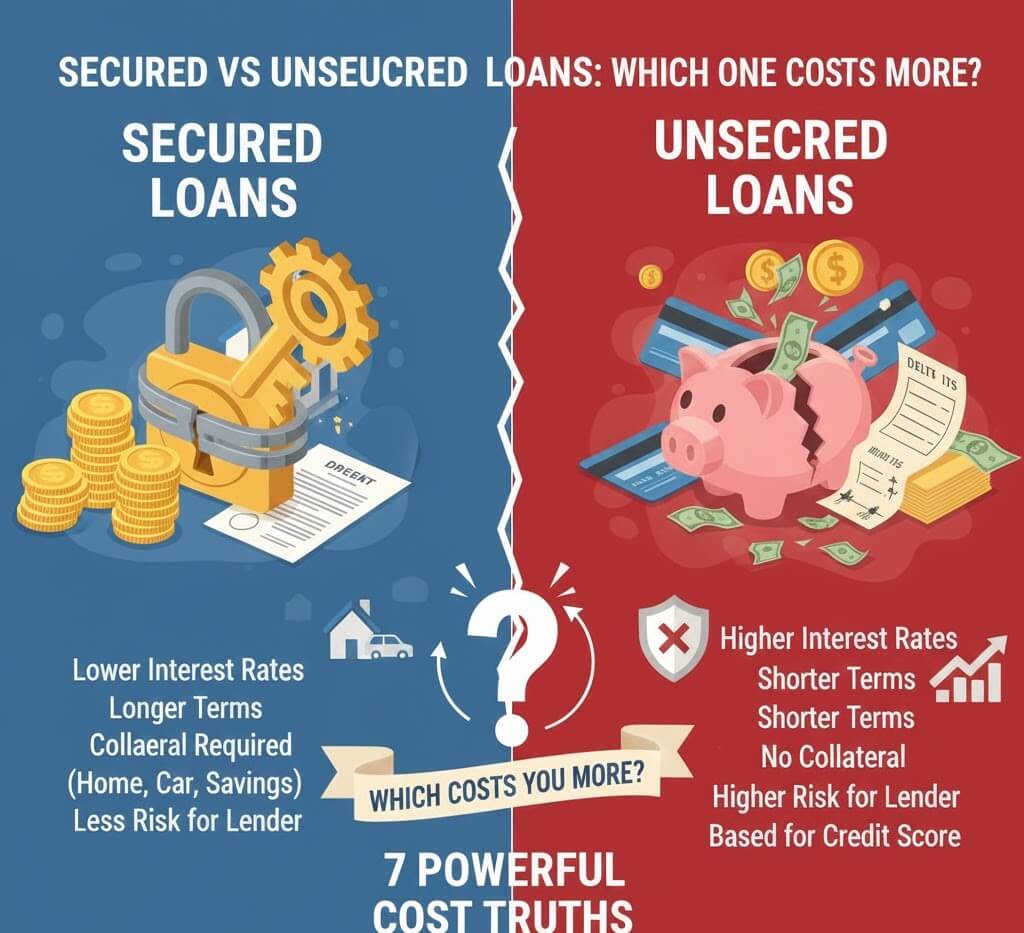

What Is a Secured Loan?

A secured loan is secured or supported by collateral; something of value that is owned by the borrower. Common examples include:

- Home loans(collateral: property)

- Auto loans (collateral: car)

- Savings, gold, or asset secured personal loans.

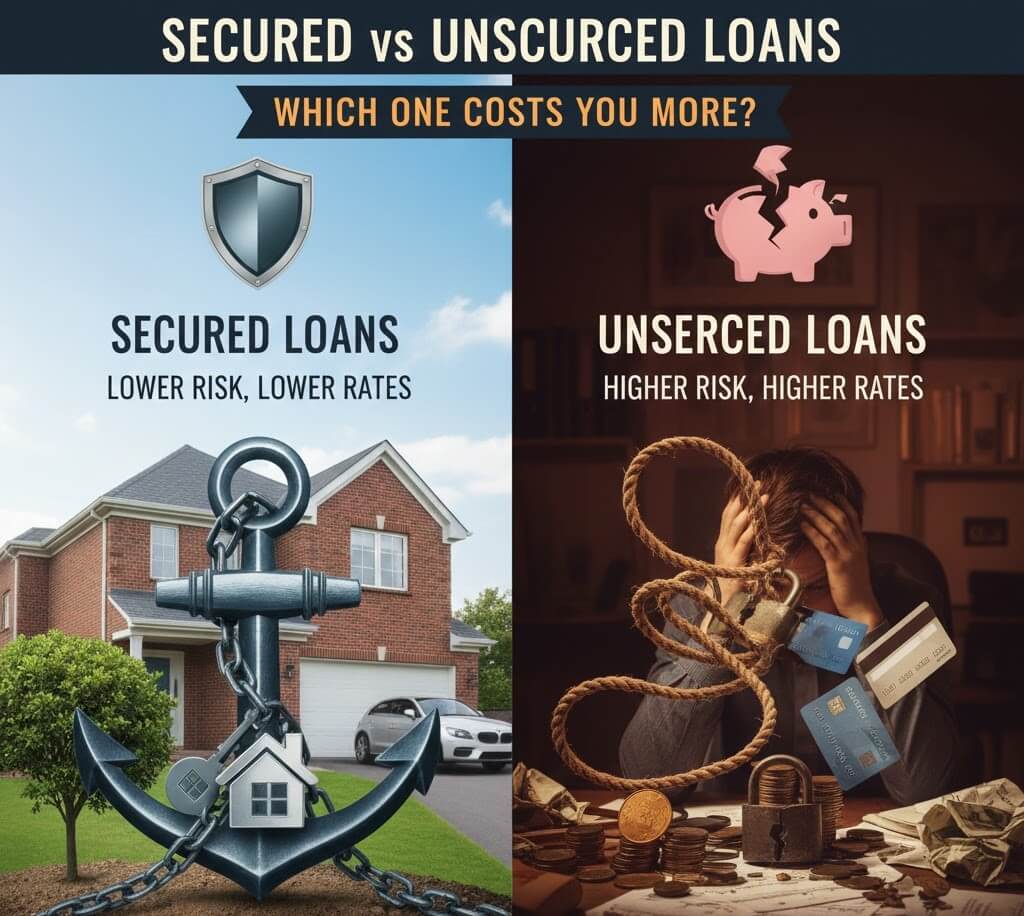

Lenders tend to be less risky withSecured vs Unsecured Loans due to the fact that the lender can take control of the collateral in case of default.

What Is an Unsecured Loan?

A personal loan does not need security. Approval is based on:

- Credit score

- Income

- Debt-to-income ratio

- Financial history

These are credit cards, personal loans and student loans. The cost structure is now altered because lenders are more risky.

The Methodology of Lenders to compute the cost of loans.

The tip on the lender pricing of loans assists in answering the question of Secured vs Unsecured Loans: Which One Costs You More?

Interest Rates Explained

The largest cost driver is the interest rates.

- Interest rates on secured loans are normally lower as collateral lessens the risk to the lender.

- Unsecured loans also have a high-interest rate particularly to average or poor credit borrowers.

A 35 percent difference can translate into the difference of thousands of dollars in time.

Over latest post:Best Credit Score Range for Personal Loans and Credit Cards Proven Guide (2025)

Fees and Hidden Charges

In addition to interest lenders can charge:

- Origination fees

- Processing fees

- Late payment penalties

- Prepayment charges

Unsecured loans will have greater origination charges whereas secured loans can have appraisal or documentation expenses that relate to collateral.

Comparison of Costs of Secured and Unsecured Loans

Short-Term Cost Differences

In the short term:

- Unsecured loans can be perceived as cheaper since they do not have an asset risk.

- But as the monthly payment is increased that convenience is often compensated.

Long-Term Financial Impact

Over the longer term, secured loans tend to prevail on cost since:

- The reduction of interest reduces slower.

- The more extended repayment period, the less pressure in the month.

e.g. a secured loan at 7 per cent in 10 years will nearly always be cheaper than an unsecured loan at 14 per cent in 5 years–how much the unsecured loan might feel expedited.

Risk, Collateral and Borrower responsibility.

There is more to cost than numbers–cost exposure.

What Happens If You Default?

- You may lose your property with a secured loan.

- Using unsecured loan, they can incur collections or lawsuit which hurts your credit in the long run.

Although secured loans are less expensive, unsecured loans can be more comfortable to some borrowers.

Over latest post:Why Credit Card Utilization Matters More Than You Think: 15 Powerful Insights

The Effect of Credit Score on the cost of a loan

The role of credit score is decisive in the case of Secured vs Unsecured Loans: Which One Costs You More?

- Good credit rating – loans which are not secured become cheaper.

- Poor credit score – restricted financing might be the sole viable alternative.

In the actual lending processes borrowers with good credit occasionally acquire unsecured loans at the same rates as the secured loans.

Application Cases and Uses in the Real World.

We can consider two simplified situations:

- Scenario A: Secured Loan

- Amount: $20,000

- Rate: 7%

- Term: 5 years

- Total cost ≈ $23,800

Scenario B: Unsecured Loan

- Amount: $20,000

- Rate: 14%

- Term: 5 years

- Total cost ≈ $27,500

That is a difference of 3,700, all because of the structure of the loan

Pros and Cons Comparison Table

| Feature | Secured Loan | Unsecured Loan |

|---|---|---|

| Interest Rate | Lower | Higher |

| Collateral Required | Yes | No |

| Approval Difficulty | Easier | Harder |

| Risk to Assets | High | None |

| Total Cost | Lower overall | Higher overall |

How to select the best loan

Ask yourself:

- Can I risk my asset?

- Am I eligible to receive low unsecured rates?

- Is cost less significant than long-term convenience in the short term?

No such thing–but the most knowledgeable borrowers always pay less.

Frequently asked questions (FAQs)

What is the overall cost of a particular type of loan?

Unsecured loans tend to be expensive with interest rates that are high.

Are loans that are secured necessarily cheaper?

Yes, at least not in every standard case, but most standard cases.

Are good credit loans cheaper than bad credit loans?

Absolutely. Good credit will help save a lot of money.

Is collateral risk at a lower interest?

It is dependent on financial stability and the significance of assets.

Are secured loans more effective at improving credit?

Both are able to enhance credit when paid in time.

Which is the best loan in cases of emergencies?

Fast but more expensive are unsecured loans.

Conclusion

In the question of Secured vs Unsecured Loans: Which One Costs You More therefore the statistical response is evident; unsecured loans tend to be costlier in terms of cost whereas secured loans tend to be riskier in personal terms. Smart borrowing is prioritizing cost, risk and intent, rather than just focusing on convenience.