How to Increase Your Credit Score Fast (Legit Methods Only)

Enhancing your credit profile does not need tricks, frauds, or dangerous shortcuts. Unless you are looking into ways of raising your credit score without resorting to felonious means, then chances are that you are seeking honest, secure, and proven advice that works. The bad news is that most people believe it takes years to improve credit scores, but the good news is that it can happen within a short period of time provided you put in the right things at the right time.

The guide is based on field experience of financial matters, best practices by lenders and data-driven information applied by banks and credit bureaus. You might be making a loan or mortgage application, credit card application or you might be simply curious what to do and what not to avoid, this article will demonstrate to you just what you need to do to get peace of mind and what to do not to.

Over latset post:Why Credit Card Utilization Matters More Than You Think: 15 Powerful Insights

How Credit Scores Work -The Real Story

Whatever you are optimizing, you need to know before you apply a tactic. Credit scores are not a secret: they are mathematical models that are aimed at risk prediction.

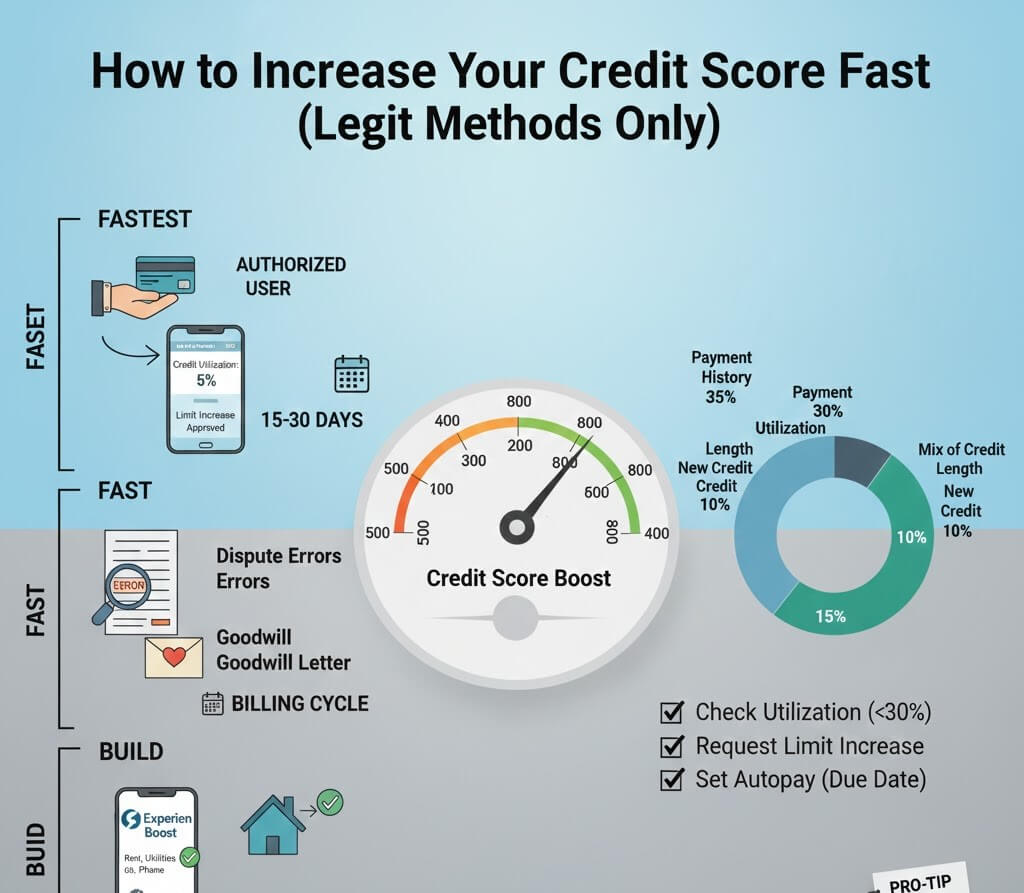

Which Factors Have the greatest Effect on your credit score?

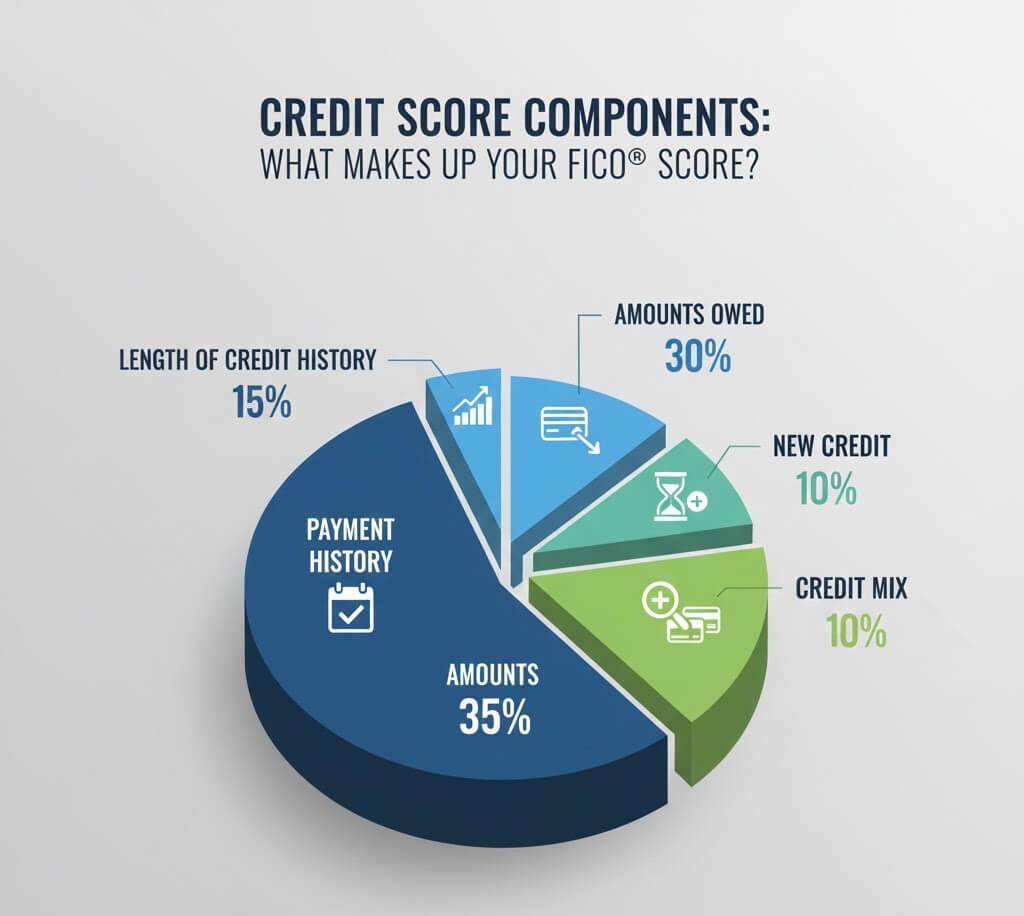

The factors in most scoring models (such as FICO 4 8 and VantageScore 3.0) have weights approximately as follows:

- Payment history (35%)

- Credit utilization (30%)

- Length of credit history (15%)

- Credit mix (10%)

- New credit inquiries (10%)

This means two things:

- Your score can be improved within a short time by emphasizing on utilization and payments.

- There are also things that require time and therefore patience is still a factor.

The reason why it is possible to make fast improvements

The credit scores are updated on a monthly basis. You can make improvements within 30-45 days in case you cut balances or eliminated mistakes today. This is why it is not a dream to learn how to raise your credit score within a short period of time (the only legitimate ways to do it).

Over latset post:Secured vs Unsecured Loans: Which One Costs You More? | 7 Powerful Cost Truths Revealed

Wrongly listed on Your Credit Reports: Check that your credit report does not show any erroneous items.

Correcting incorrect data is one of the quickest and legitimate methods of getting a higher score.

Typical Report Credit Report Follies.

- Accounts you don’t recognize

- Actually timely payment that was late.

- Missing balances and credit limits.

- Duplicate accounts

- Closed accounts that are open marked.

A report by the Consumer Finance research revealed that 1 out of 5 credit reports has an error that would have a scoring impact.

The manner in which to confront mistakes.

- Get reports out of all the big bureaus.

- Online highlight false entries.

- Present disagreements in the form of documents.

- Follow up within 30 days

Over latset post:Auto Insurance Explained: What Coverage Do You Actually Need? | Ultimate 2025 Guide

Step 2: Strategically Pay Off You Credit Card Balances.

This step will only be able to bring about rapid increases of scores.

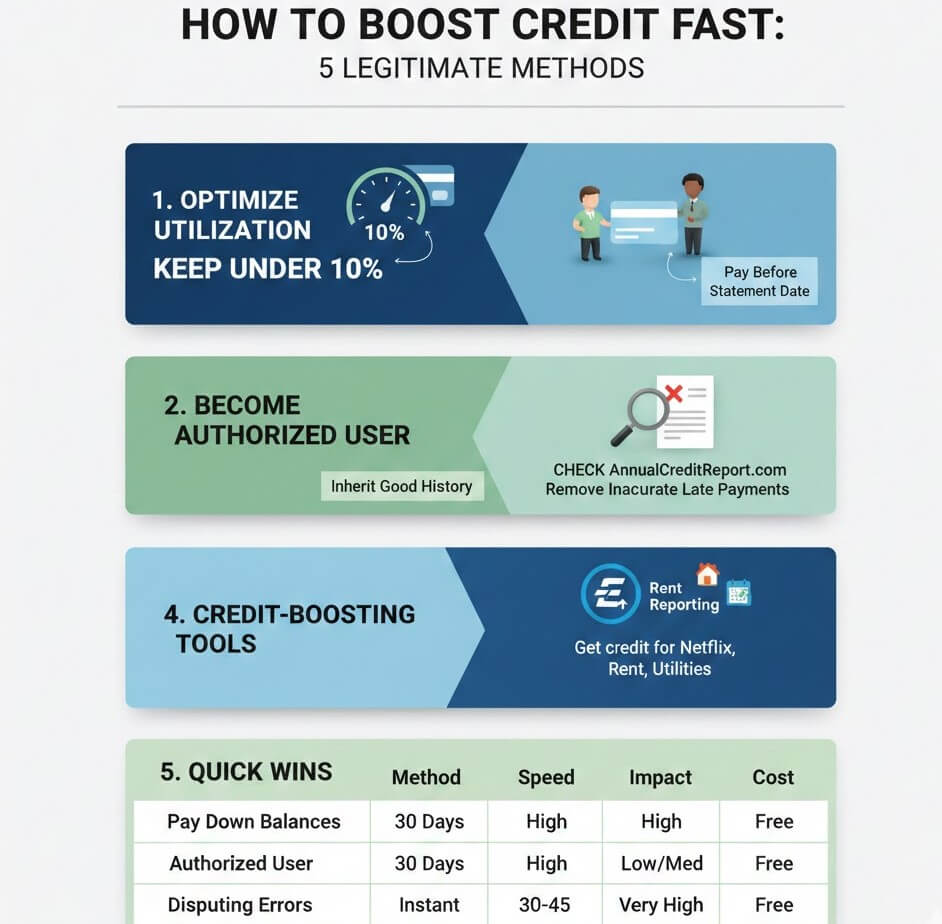

Credit Utilization Ratio Understanding

- Credit utilization =

Total credit card balances/ Total credit limits - Reduced utilization is an indicator of reduced risk to the lenders.

The 30%, 10%, and 1% Rule

- Under 30%: Minimum acceptable

- Under 10%: Excellent

- 1-5%: Optimal for fast score gains

Trick of the trade: Pay balances prior to statement closing dates- not due dates.

Step 3: Never Miss a Payment (Even Once).

The best weight is on payment history.

Payment History Explained

A single late payment may remain on your report of 7 years. A 30 days late will even demerit you by 60-100 points.

Protective Automations on your Score.

- Money auto-pay minimum.

- Use calendar reminders

- Enable bank alerts

- Perfection is nothing to consistency.

Over latset post:Credit Score vs Credit Report: What Banks Actually Check – Powerful Guide 7

Strategy 4: Authorized User Strategy.

This is among the strongest yet misconstrued strategies.

The way Authorized Users Improve Scores.

To be added to an account managed:

- You inherit its age

- It has the advantage of a good payment record.

- It makes you score well in utilization.

Risks and Best Practices

Only join accounts with:

- Low balances

- Long history

- Perfect payment record

Cards that are risky or maxed should be avoided.

Step 5: Do Not ask New Hard Questions.

Hard vs Soft Credit Checks

- Hard questions: Influence your rating.

- Soft inquiries: No impact

A single hard pull can deduct between 3-7 points.

Hint: You should not rebuild with useless applications.

Step 6: Keep Old Accounts Open

History of Credit Length Matters.- Older accounts raise your average account age, and this raises trust signals in your scoring models.

- Close old cards unless they are charged an annual fee.

Step 7: Use Credit Mix Wisely

Installment Credit vs. Revolving Credit.

A healthy mix may include:

- Credit cards

- Personal loans

- Auto loans

You need not be able to have it all, you need to balance.

Step 8:Take credit builder tools into account.

Secured Credit Cards and Credit Builder Loans.

These are aimed at the improvement of the score:

- Small deposits

- Low risk

- Reported monthly

They burn slowly–but they burn.

Step 9: Trace the Progress and Be Consistent.

Surveillance enables you to identify change early enough and adapt.

- Check monthly updates

- Watch utilization changes

- Celebrate small wins

- Improvement is cumulative.

Frequently Asked Question (FAQs).

What is the best rate at which my credit score can be raised?

You can expect results in 30-60 days in case you minimise balances and correct mistakes.

Will the instant score boost be achieved by paying off debt?

Yes- particularly credit cards, because there was utilization change.

Is my credit score lessening because of checking my credit?

No. It is a tender enquiry to check your own report.

Is it worth using credit repair companies?

Majority of their actions are something you can do by yourself- free.

Is it advisable to close idle credit card?

No, not normally, unless it has a high annual fee.

Does it ensure a sure method of achieving an 800?

There are no assurances–but regular good practices can accomplish it.

Verdict: Sustainable Growth of Credit Carries the Day

It is a question of smart prioritization, not shortcuts, to learn how to raise your credit score in a short period (only the legitimate ways). Pay attention to accuracy, use, discipline in payment and patience. Also, do this regularly and you will be rewarded by your credit score.